Government Debt, deficit and Policy Issues - Macroeconomics

Is government debt a problem?

There are two parts to a question of government debt:

1. Deficit

2. Debt

The deficit matters as it adds to the stock of debt. Questions about the sustainability of government debt are expressed as a ratio to GDP (national income)

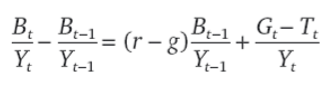

Government debt is the accumulation of current and past deficits. Debt owned by government equals stock of bonds B(t). The budget deficit is the difference between expenditures, which includes any interest on the debt it owes, and its receipts (mostly from tax)

The first term is the real interest paid on government bonds in circulation. G(t) is the government spending on goods and services in year t. T(t) are taxes less transfers in year t. The difference between (G-T) is known as the primary deficit.

This equation tells us that the change in the debt ratio is equal to the sum of two terms:

This equation tells us that the change in the debt ratio is equal to the sum of two terms:

1. The first is the difference between the real interest rate and the rate of growth of GDP, multiplied by the debt ratio at the end of the previous period

2. The second term is the ratio of the primary deficit to GDP

To capture trends in the debt we want to study its evolution, holding r, g and primary deficit constant

We assume that the government runs primary deficits (or surpluses) in relation to GDP that is constant over time. We also assume that r and g are constant.

Two main cases can arise:

1. The normal case - on most occasions, the growth rate of GDP is smaller than the real interest rate. The equation is a straight line with a slope greater than 1. r>g, explosive national debt and unsustainable deficit.

2. The more exotic case - less frequent, it can happen that the GDP growth rate exceeds the real interest rate. The equation is then described by a straight line with a slope lower than 1 (1+r+g < 1). r<g, stable national debt and sustainable deficit.

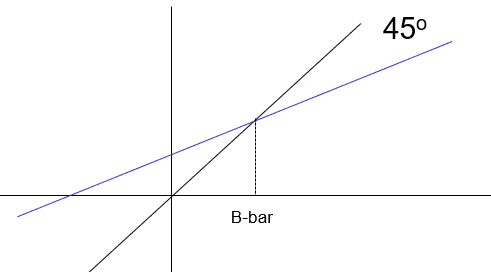

EVOLUTION OF THE DEBT/GDP RATIO

1. Explosive debt becoming unaffordable

The X axis is debt at t-1. Y-axis is debt at t. Here we see that g < r (slope is steep) and if the country has past debt and runs primary deficits (G-T > 0) - intercept is positive, then the debt ratio increases going farther away from equilibrium. Further, it can be seen that the intersection point representing the equilibrium lies in the 3rd quarter, that is, at equilibrium government would run a net surplus. However, the equilibrium is unstable and the economy would not be able to sustain that point.

2. Explosive debt becoming affordable

Even if g < r (slope is steep), and if the initial debt is positive, the debt ratio decreases over time if the government runs adequate primary surpluses (G-T < 0), negative intercept. It can be seen that the equilibrium point is in the first quadrant and the economy can sustain some positive debt, however, again the point is unsustainable. Although the debt is explosive, by running a fiscal surplus the debt can become affordable with time.

3. Stable debt but is it affordable?

The government must increase the debt by a factor of (1+r) to pay the interest on the outstanding stock of bonds. But the GDP is increasing at rate 1+g, expanding the capacity of the government to generate revenues. This factor makes the debt-to-GDP ratio growing more slowly. If g > r, the debt ratio converges to the equilibrium level despite the presence of primary deficits (G-T > 0). So, the government can sustain some debt alongside running a fiscal deficit.

4. Stable debt, affordable?

If g > r and the government runs primary surpluses (G - T < 0 ), then the debt ratio always converges to its equilibrium level.

To make things simple in the diagrams we kept deficit, growth and interest rate constant. In practice, they move around.

The recent experience of some European countries with a debt ratio above 100% shows the risk of a vicious circle. To increase the primary surplus, the government raises taxes, but tax hikes are unpopular and subsequently lead to a reduced rate of growth. The increase in the interest rate and the lower growth rate result in higher r-g, making it even more difficult to stabilise the debt ratio. It is therefore clear that countries with high debt should reduce it rapidly.

If the stock of public debt, as a ratio to GDP, reaches a very high level, the situation can escalate and lead to a debt crisis. For instance: the government finds it impossible to issue new debt, except at extraordinarily high interest rates. But governments do not perceive the urgency of an adjustment to avoid losing political consensus and thereby opening social conflicts.

How to reduce high debt? The same old methods:

1. Generate sufficient primary surpluses

2. Resort to monetary financing by the central bank

3. Repudiate the debt

POLICY ISSUES

1. Ricardian Equivalence:

Ricardian equivalence, further developed by Robert Barro, is the argument that once the government budget constraint is taken into account, neither deficit nor debt has an effect on economic activity. The consumers do not change their consumption in response to a tax cut if the present value of after-tax labour income is unaffected. The effect of lower taxes today is cancelled out by higher taxes tomorrow. However, empirically it does not hold true.

If households do not have access to credit markets or if the credit markets are not properly developed then the households may face problem in bringing their future wealth to the present for consumption. Under such situations, policies may impact present consumption and distort the pattern.

2. Time inconsistency:

We have assumed so far that all economic agents (firms, households and governments) share the same objective function (they care about inflation, output and employment). In practice, the objective function of firms/ households versus government and central banks may differ. This might be exploited, to engineer a boom close to elections for example. This deviation is bad for the economy since it creates unnecessary booms and busts. This incentive to deviate is known as time-inconsistency.

3. Fiscal Rules:

If politics sometimes lead to long and lasting budget deficits, can rules be put in place to limit these adverse effects?

1. One approach tried in the USA is to use a constitutional amendment to balance the budget.

2. A better approach is to put in place rules that put limits on either deficits or debt.

3. A complementary approach is to put in place mechanisms to reduce deficits, were such deficits to arise

4. The labour government specified two key fiscal rules that provide benchmarks against which the performance of fiscal policy can be judged: the golden rule and the sustainable investment rule

4. Monetary Policy Rule:

Most central banks have adopted an inflation rate target rather than a nominal money growth target and, they think about short-run monetary policy in terms of movements in the nominal interest rate rather than in terms of movements in the rate of nominal money growth. These are commonly known as Taylor rules. The CB does not act using a Taylor rule, but rather appears to act as if it was using one. This rule can be built into the dynamic model and relates to the discussion about money growth in that model.

According to the Taylor rule, since it is the interest rate that directly affects spending, the CB should choose an interest rate rather than a rate of nominal money growth.

Taylor's rule provides a way of thinking about monetary policy: once the central bank has chosen a target rate of inflation, it should try to achieve it by adjusting the nominal interest rate.

Can think of i* in the dynamic AD-AS model as choosing the growth rate of the money stock to achieve a certain nominal interest rate in the medium run (a constant g_m).

There are two parts to a question of government debt:

1. Deficit

2. Debt

The deficit matters as it adds to the stock of debt. Questions about the sustainability of government debt are expressed as a ratio to GDP (national income)

Government debt is the accumulation of current and past deficits. Debt owned by government equals stock of bonds B(t). The budget deficit is the difference between expenditures, which includes any interest on the debt it owes, and its receipts (mostly from tax)

The first term is the real interest paid on government bonds in circulation. G(t) is the government spending on goods and services in year t. T(t) are taxes less transfers in year t. The difference between (G-T) is known as the primary deficit.

1. The first is the difference between the real interest rate and the rate of growth of GDP, multiplied by the debt ratio at the end of the previous period

2. The second term is the ratio of the primary deficit to GDP

To capture trends in the debt we want to study its evolution, holding r, g and primary deficit constant

We assume that the government runs primary deficits (or surpluses) in relation to GDP that is constant over time. We also assume that r and g are constant.

Two main cases can arise:

1. The normal case - on most occasions, the growth rate of GDP is smaller than the real interest rate. The equation is a straight line with a slope greater than 1. r>g, explosive national debt and unsustainable deficit.

2. The more exotic case - less frequent, it can happen that the GDP growth rate exceeds the real interest rate. The equation is then described by a straight line with a slope lower than 1 (1+r+g < 1). r<g, stable national debt and sustainable deficit.

EVOLUTION OF THE DEBT/GDP RATIO

1. Explosive debt becoming unaffordable

The X axis is debt at t-1. Y-axis is debt at t. Here we see that g < r (slope is steep) and if the country has past debt and runs primary deficits (G-T > 0) - intercept is positive, then the debt ratio increases going farther away from equilibrium. Further, it can be seen that the intersection point representing the equilibrium lies in the 3rd quarter, that is, at equilibrium government would run a net surplus. However, the equilibrium is unstable and the economy would not be able to sustain that point.

2. Explosive debt becoming affordable

Even if g < r (slope is steep), and if the initial debt is positive, the debt ratio decreases over time if the government runs adequate primary surpluses (G-T < 0), negative intercept. It can be seen that the equilibrium point is in the first quadrant and the economy can sustain some positive debt, however, again the point is unsustainable. Although the debt is explosive, by running a fiscal surplus the debt can become affordable with time.

3. Stable debt but is it affordable?

The government must increase the debt by a factor of (1+r) to pay the interest on the outstanding stock of bonds. But the GDP is increasing at rate 1+g, expanding the capacity of the government to generate revenues. This factor makes the debt-to-GDP ratio growing more slowly. If g > r, the debt ratio converges to the equilibrium level despite the presence of primary deficits (G-T > 0). So, the government can sustain some debt alongside running a fiscal deficit.

4. Stable debt, affordable?

If g > r and the government runs primary surpluses (G - T < 0 ), then the debt ratio always converges to its equilibrium level.

To make things simple in the diagrams we kept deficit, growth and interest rate constant. In practice, they move around.

The recent experience of some European countries with a debt ratio above 100% shows the risk of a vicious circle. To increase the primary surplus, the government raises taxes, but tax hikes are unpopular and subsequently lead to a reduced rate of growth. The increase in the interest rate and the lower growth rate result in higher r-g, making it even more difficult to stabilise the debt ratio. It is therefore clear that countries with high debt should reduce it rapidly.

If the stock of public debt, as a ratio to GDP, reaches a very high level, the situation can escalate and lead to a debt crisis. For instance: the government finds it impossible to issue new debt, except at extraordinarily high interest rates. But governments do not perceive the urgency of an adjustment to avoid losing political consensus and thereby opening social conflicts.

How to reduce high debt? The same old methods:

1. Generate sufficient primary surpluses

2. Resort to monetary financing by the central bank

3. Repudiate the debt

POLICY ISSUES

1. Ricardian Equivalence:

Ricardian equivalence, further developed by Robert Barro, is the argument that once the government budget constraint is taken into account, neither deficit nor debt has an effect on economic activity. The consumers do not change their consumption in response to a tax cut if the present value of after-tax labour income is unaffected. The effect of lower taxes today is cancelled out by higher taxes tomorrow. However, empirically it does not hold true.

If households do not have access to credit markets or if the credit markets are not properly developed then the households may face problem in bringing their future wealth to the present for consumption. Under such situations, policies may impact present consumption and distort the pattern.

2. Time inconsistency:

We have assumed so far that all economic agents (firms, households and governments) share the same objective function (they care about inflation, output and employment). In practice, the objective function of firms/ households versus government and central banks may differ. This might be exploited, to engineer a boom close to elections for example. This deviation is bad for the economy since it creates unnecessary booms and busts. This incentive to deviate is known as time-inconsistency.

3. Fiscal Rules:

If politics sometimes lead to long and lasting budget deficits, can rules be put in place to limit these adverse effects?

1. One approach tried in the USA is to use a constitutional amendment to balance the budget.

2. A better approach is to put in place rules that put limits on either deficits or debt.

3. A complementary approach is to put in place mechanisms to reduce deficits, were such deficits to arise

4. The labour government specified two key fiscal rules that provide benchmarks against which the performance of fiscal policy can be judged: the golden rule and the sustainable investment rule

4. Monetary Policy Rule:

Most central banks have adopted an inflation rate target rather than a nominal money growth target and, they think about short-run monetary policy in terms of movements in the nominal interest rate rather than in terms of movements in the rate of nominal money growth. These are commonly known as Taylor rules. The CB does not act using a Taylor rule, but rather appears to act as if it was using one. This rule can be built into the dynamic model and relates to the discussion about money growth in that model.

According to the Taylor rule, since it is the interest rate that directly affects spending, the CB should choose an interest rate rather than a rate of nominal money growth.

Taylor's rule provides a way of thinking about monetary policy: once the central bank has chosen a target rate of inflation, it should try to achieve it by adjusting the nominal interest rate.

Can think of i* in the dynamic AD-AS model as choosing the growth rate of the money stock to achieve a certain nominal interest rate in the medium run (a constant g_m).

Comments

Post a Comment